Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Amidst recent chatter about the economy and concerns about a potential recession, many are wondering if a housing market crash is on the horizon, especially in the Cincinnati and northern Kentucky real estate markets. It’s natural to be concerned, but rest assured—the current housing market is not poised for a crash.

Real estate journalist Michele Lerner defines a housing market crash as occurring “when home values plummet due to a lack of demand for homes or an oversupply.” With this definition in mind, let’s look at two key reasons why a crash is unlikely in today’s real estate market, especially in our Cincinnati and northern Kentucky communities.

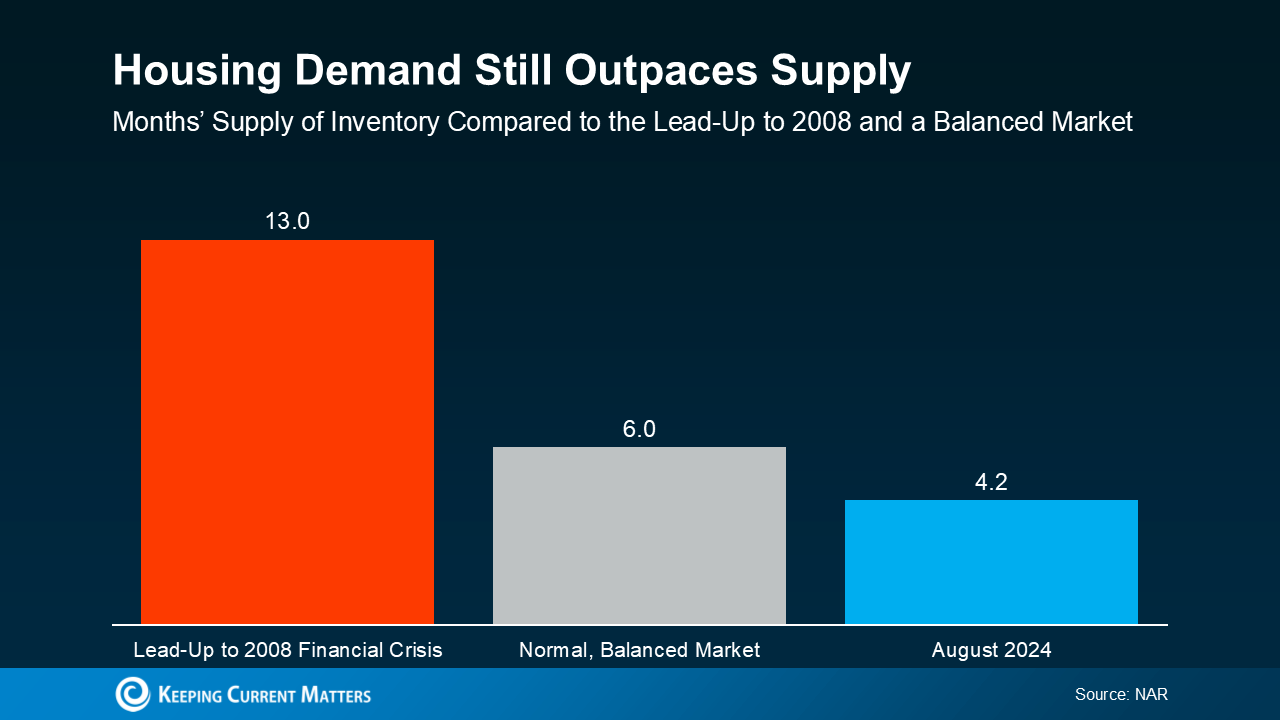

### 1. Demand for Homes in Cincinnati and Northern Kentucky Is Outpacing Supply

One of the major reasons for the 2008 housing market crash was an oversupply of homes. But today’s situation, including in the greater Cincinnati and northern Kentucky areas, is quite different.

A balanced real estate market generally has a six-month supply of homes, where supply and demand are equal. If the supply exceeds six months, it suggests an oversupply, and if it’s lower, demand is outpacing supply. Data from the National Association of Realtors (NAR) shows that in today’s market, supply is much lower than demand—currently around 4.2 months nationwide. Locally, Cincinnati and northern Kentucky continue to experience a shortage of available homes, keeping the market competitive and stable.

The graph below highlights these trends:

Lawrence Yun, Chief Economist at NAR, emphasizes the stability, stating: “We simply don’t have enough inventory. While some markets may see a slight price decline, a dramatic 30 percent drop like in 2008 is highly unlikely.” This rings true in our local Cincinnati and northern Kentucky real estate markets, where demand continues to drive the market.

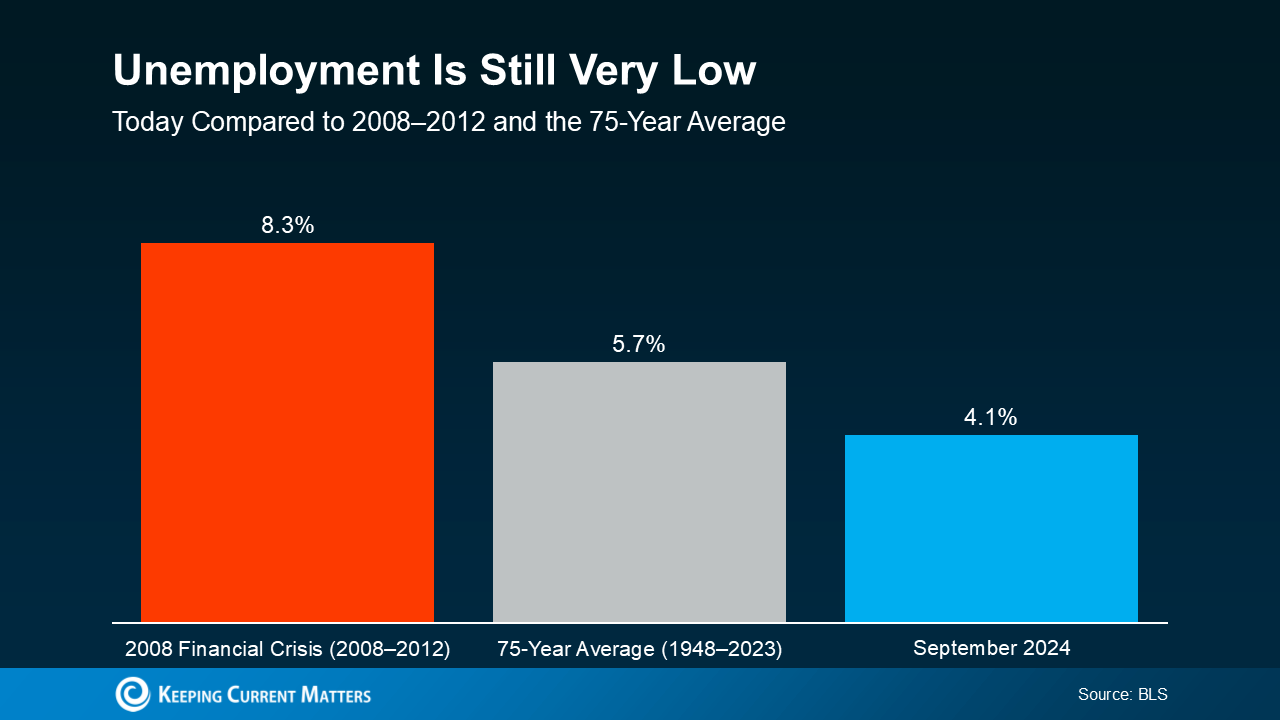

### 2. Low Unemployment Bolsters Market Stability

Unemployment is another factor that greatly influences the housing market. In 2008, high unemployment rates led to widespread foreclosures as homeowners struggled to make mortgage payments. Today, however, the employment landscape is much stronger, both nationally and locally in Cincinnati and northern Kentucky.

The graph below shows a stark comparison of unemployment rates across three key periods:

As of now, the unemployment rate is 4.1%, far below the 8.3% seen during the 2008 financial crisis. People are working, paying their mortgages, and in many cases, buying homes, which keeps demand—and prices—up. The employment strength in our local Cincinnati and northern Kentucky economies further supports the health of our real estate markets.

### Cincinnati and Northern Kentucky’s Housing Market Is Stronger than in 2008

Concerns about economic uncertainty and recession are understandable, but today’s real estate market, especially in areas like Cincinnati and northern Kentucky, is far more resilient than in 2008. According to Rick Sharga, Founder and CEO of CJ Patrick Company, “Literally everything is different about today’s housing market dynamics than the conditions that led to the housing crisis.”

With demand outpacing supply and unemployment remaining low, there is little indication that the housing market will crash in the foreseeable future.

### Bottom Line

While the overall housing market is in a stronger position than it was in 2008, remember that real estate is always local. Cincinnati and northern Kentucky communities are experiencing healthy demand, limited supply, and steady employment—factors that help keep the real estate market stable.

If you have questions about how the national economic trends are affecting our local market, or if you’re thinking about buying or selling in Cincinnati or northern Kentucky, it’s always wise to consult with a knowledgeable local real estate agent. We’re here to help you navigate today’s market with confidence.